On Thursday, Polymarket handed its critics the sharpest argument yet.

A governance vote coordinated through UMA has settled a heavily traded market as “No”, meaning MicroStrategy did not sell Bitcoin by May 31, even though Strategy’s own SEC filing confirms it sold 32 BTC between May 26 and May 31. The catch? That filing did not drop until June 1, one day after the contract expired.

What followed has shaken confidence in one of crypto’s most prominent prediction platforms, and the debate it has triggered goes well beyond one disputed market.

Contents

The Market, The Filing, and The One-Day Gap That Changed Everything

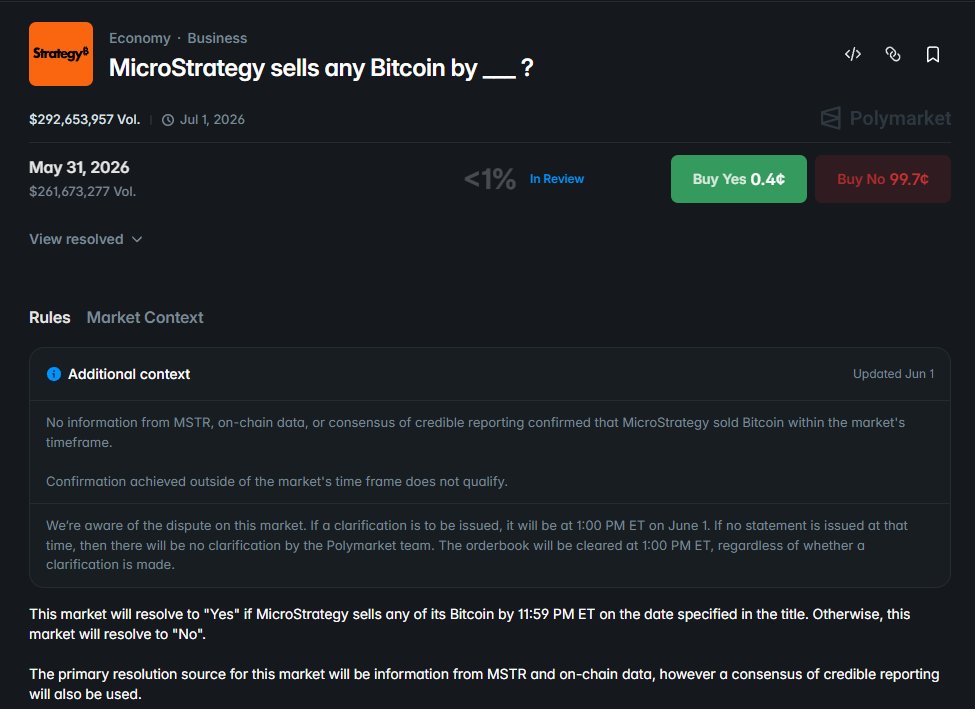

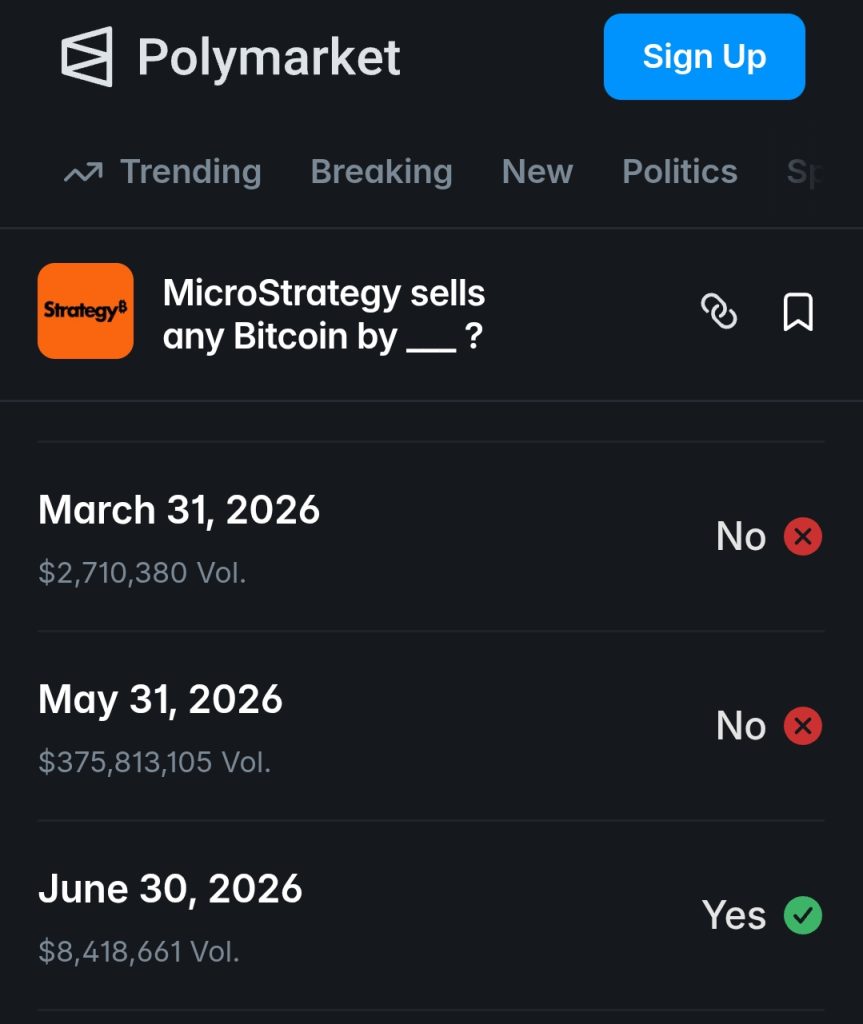

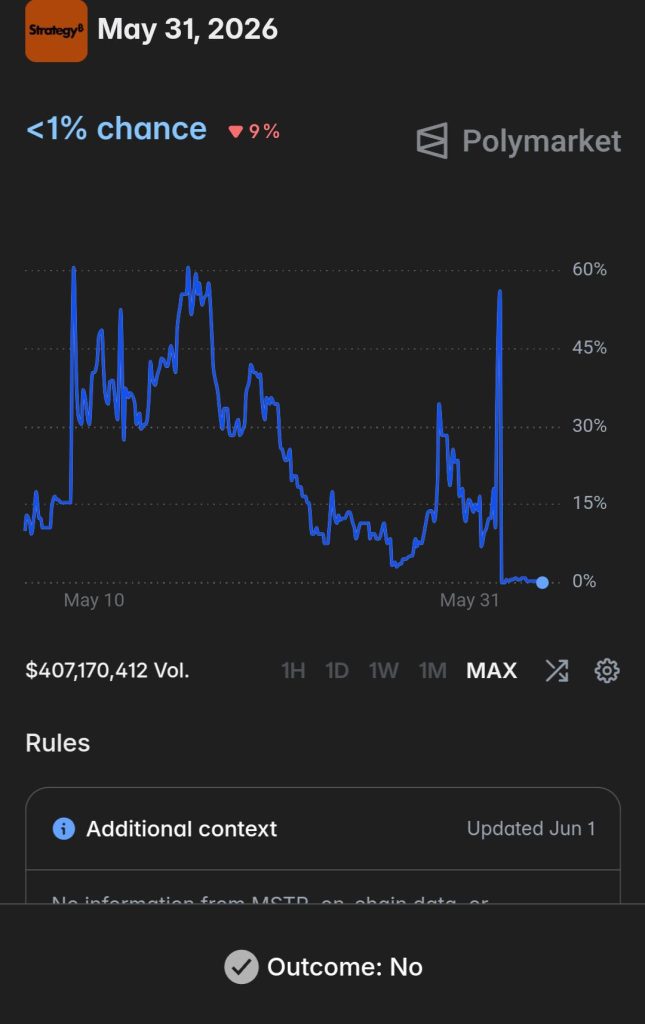

The Polymarket contract asked a straightforward question: did MicroStrategy sell any Bitcoin by May 31, 2026? Based on what was publicly available before the deadline, Polymarket’s resolution process determined the answer was no.

Strategy’s 8-K disclosure confirming the sale of 32 BTC only became public on June 1, twenty-four hours after the market window closed.

Strategy’s 8-K disclosure confirming the sale of 32 BTC only became public on June 1, twenty-four hours after the market window closed.

Polymarket leaned on that technicality. The platform argued that no verified information confirmed a sale within the market’s active timeframe, and it issued a clarification to that effect after noticing heavy “Yes” buying in the contract’s final hours. That clarification, and the timing of it, is where things get complicated.

The underlying facts are not in dispute. Strategy sold Bitcoin. It sold it between May 26 and May 31, squarely within the contract period. The sale happened. It simply was not publicly confirmed via SEC filing until the following morning. Whether that distinction is a principled legal boundary or a convenient loophole is the question tearing the Polymarket community apart right now.

Polymarket Traders Are Claiming Losses

The fallout has been swift and angry. One pseudonymous trader operating under the name willo2 claims to have lost approximately $500,000 on the “Yes” side of the trade. Another affected user has reportedly issued a formal legal demand against the platform, a rare escalation that signals just how seriously some participants are taking the outcome.

1/ @Polymarket's contested market on whether @Strategy sold #Bitcoin by 31 May settled as 'No' on 4 June, even though Strategy disclosed selling 32 $BTC between 26 and 31 May.

The difference: the SEC filing didn't drop until 1 June, one day after the contract expired.

— Sandmark (@sandmark_news) June 4, 2026

These are not casual bettors upset about a bad call. They are sophisticated market participants who read the SEC filing, understood what it meant, and placed significant capital on what they believed was a factual outcome. The filing confirmed the sale. The market said it did not happen. From their perspective, the platform changed the rules after the game was already played.

The “Yes” buyers had a reasonable case. Strategy’s own mandatory regulatory disclosure, the kind of document companies file precisely because the information is material and must be made public, confirmed the sale occurred within the contract window. The argument that this does not count because the filing arrived one day late is, to many of them, a distinction without a difference.

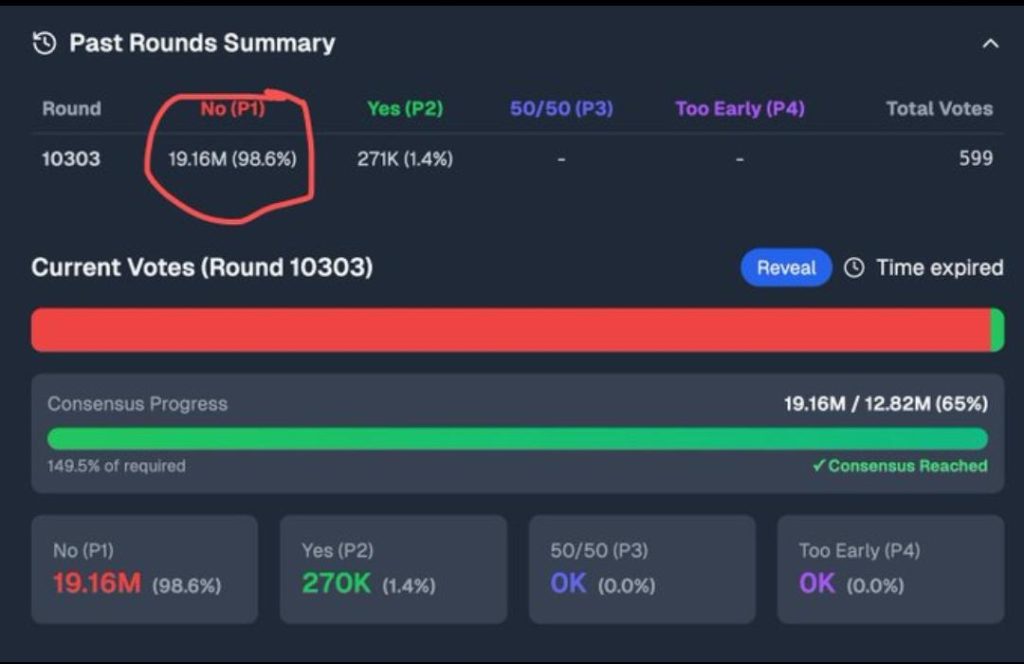

UMA Governance Vote Followed the Official Line

The resolution went through UMA’s decentralized governance mechanism, which is the system Polymarket relies on to settle disputed markets. In theory, UMA token holders vote independently to determine outcomes.

5/n

在这几天的 UMA 投票里,大户们以绝对的票数,选择了 No。这意味 polymarket 官方通过澄清的方式,引导大户们来投票。大户们为了规避风险,直接选择最简单的模式-跟随官方。这游戏没法玩了。规则不清晰,就算了。当结算要确认,官方下场开始澄清就改变了规则。

总之,游戏规则都是官方说了算! pic.twitter.com/gfofyncLDu

— 神秘极客 (@geekwho_ai) June 4, 2026

In practice, observers watching this particular vote noticed that whale voters, those holding enough tokens to meaningfully influence the result, overwhelmingly sided with “No,” following the clarification that Polymarket’s official team had issued.

The criticism from within the community cuts directly at how that process unfolded. The argument being made by a growing number of X users is that Polymarket’s team effectively guided the outcome by issuing a clarification that gave large token holders a clear signal on which way to vote. The whales, facing uncertainty and not wanting to take on risk, simply followed the official position. The vote produced the result the platform’s clarification pointed toward.

That is a damaging accusation for a system that derives its value from being censorship-resistant and manipulation-proof. If the team can issue a clarification mid-dispute that steers whale voters toward a preferred outcome, the decentralization is largely cosmetic.

The Whole Industry Is Now Watching Polymarket Now

Strip away the specific figures and the trader losses, and what this case actually establishes is a foundational question that prediction markets have never had to answer cleanly before: does a contract settle on when an event occurs, or on when that event becomes publicly verifiable?

It is not a trivial distinction. Financial markets, legal contracts, and insurance policies all grapple with similar questions around knowledge, disclosure, and timing. Polymarket has now effectively ruled that public verifiability is what controls, not the underlying event itself. If Strategy had filed its 8-K on May 31 instead of June 1, the outcome would presumably have been “Yes.” The sale was identical either way.

For bettors trying to price real-world events on Polymarket going forward, this creates a new layer of uncertainty. It is no longer enough to know what happened. You now need to know exactly when the confirming documentation becomes public, and hope that the platform does not issue a last-minute clarification that reframes the question entirely.

Disclosure: This is not trading or investment advice. Always do your research before buying any cryptocurrency or investing in any services.

Follow us on Twitter @nulltxnews to stay updated with the latest Crypto, NFT, AI, Cybersecurity, Distributed Computing, and Metaverse news!