Not without an ample dose of skepticism, 2018 can indeed be referred to as the year of the stablecoin. Amid total backlash against Tether, and yet high demand for stable cryptocurrency as a means of settlement, a growing cohort of stable coin solutions were rolled out to the market. These appear to be the stablecoins that enjoy most credibility among crypto exchanges today: Paxos Standard PAX, Gemini GUSD, Circle USDC, Carbon CUSD, TrustToken’s TUSD. Yet, it’s safe to say that none of the above products is truly decentralized, essentially being more of a token with the right to claim a fiat USD equivalent stored in a centralized storage (most often on a bank account).

What it means is that the use of those coins is linked to the same array of difficulties as those of conventional fiat money, i.e. while their value is guaranteed by the emittent, their use is most often than not accompanied by complicated KYC/AML procedures, with the risk of bank accounts being suspended due to the coins considered as ‘illegally acquired’. Hence, the use of the majority of stablecoins is completely irrational in financial services of Web 3.0., or the ‘free Internet’, since it implies a significant amount of risks. It’s safe to suggest that in a perfect world a stable means of payment for Web3 should be emitted by the community, with its value regardless of actions of the third parties.

Today it seems that the only stable coin that is securely emitted in a decentralized manner is MakerDAO’s DAI. It is also one of the most popular #DeFi apps in Ethereum ecosystem. What is it that makes DAI so unique generating an explosive amount of community trust? Here we will touch upon the core mechanics of MakerDAO emission system, and shed some light on how you as a Ethereum user can benefit from that today.

MakerDAO concept – how does a decentralized stable coin operate?

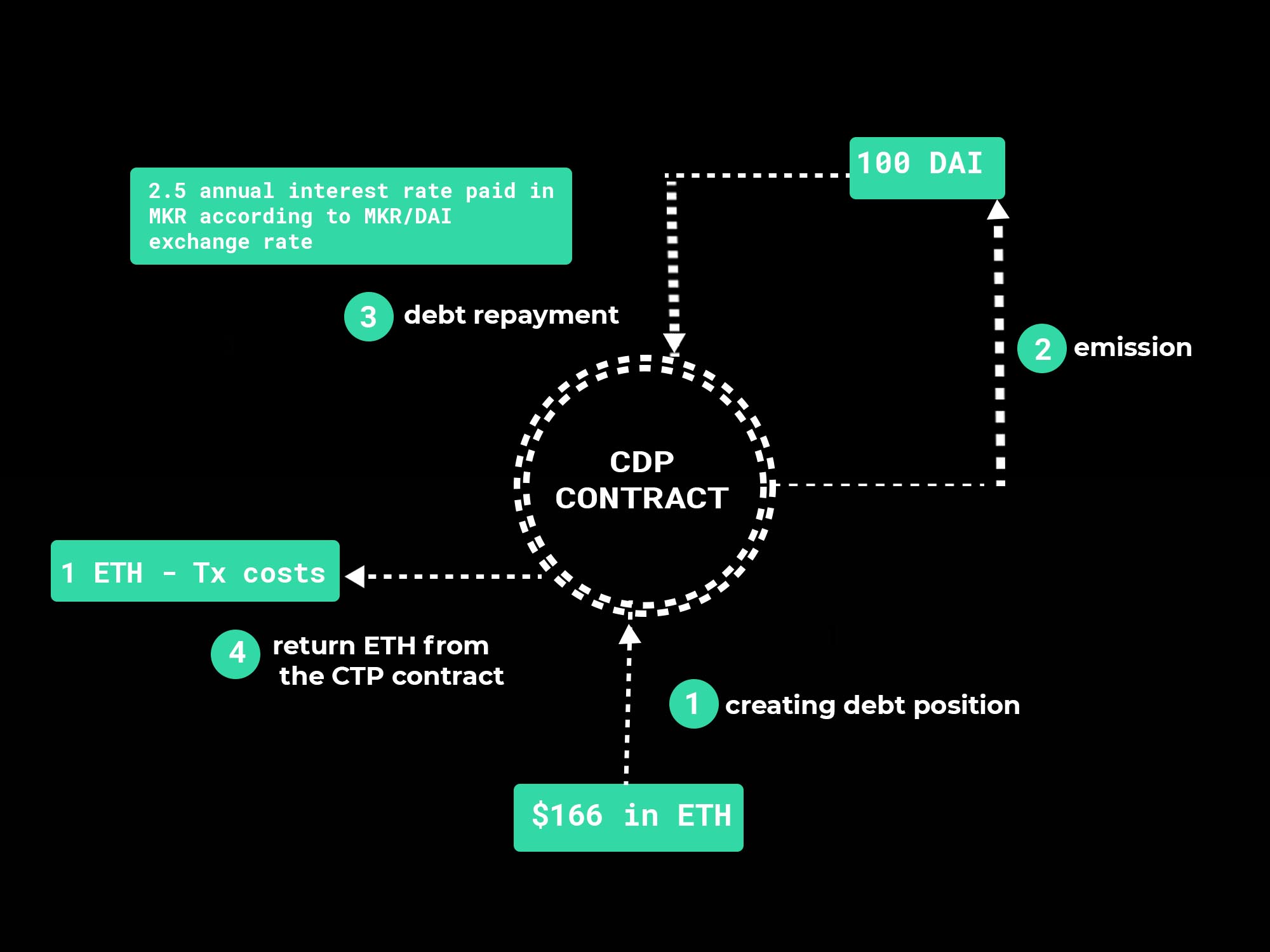

In essence, at the core of MakerDAo product is the mechanics of emission of a stable means of payment (i.e. money) deployed as a number of smart contracts in Ethereum network. In principle, the scheme of emission is akin to that of money emission secured by gold, with ETH taking the place of gold here. A specific amount of ETH is sent to a smart contract that generates a stable token (DAI), and then sends it to the user. DAIs created in this manner become the debt outstanding to MakerDAO (that in itself becomes a decentralized emission system) secured by the collateral – in exact same manner as traditional fiat money is essentially debt outstanding to a central bank. However, in contrast to traditional central banks, with DAI any user can create new decentralized money without any obstacle. At the same time, due to complete automation of MakerDAO system by design, it’s impossible to create money not secured by ETH, and the system is completely transparent to monitor.

An elephant in the room is how would DAI actually secure the stability of DAI exchange rate of $1? The concept of excessive consumption comes into play here. When emitting DAI, the secured collateral should be no less than %166, i.e. the debt in the amount of 100 DAI should be emitted to each $166. The emission made by an individual user becomes a CDP, or a collateralized debt position, each of which can be monitored on a dedicated web-page. When ETH price drops, provided that the index of position coverage drops below 150%, the position will start to liquidate. And the collateral asset, i.e. ETH, is sold at the discount for DAI that are used to cover the debt. The recent drop in ETH price from $200 to $86 over a short time span resulted in the mass close up of the debt positions due to the insufficient coverage ratio, yet DAI exchange rate stuck to ~$1.00, which confirms the high level of system stability.

DAI Emission Cycle

More so, the community trust in DAI is extremely high. According to the latest data points, the system has accumulated enormous amount of 1.7 million of ETH, or USD 255 million, as the collateral (which makes up >1.5% of all the ETH existing at the moment). More than 70 million DAI has been generated so far, which equals to ~$70 million of stable coins, with the total of collateral coverage amounting to 370%. Many dApps are also integrating DAI to provide their users with the option to make settlements in stable currency.

There is another token used in MakerDAO system – a Maker token – designated to give a voting right, when managing percentage stakes (since DAI emission is akin to the emission of conventional money with its borrowing rate), and used to pay off the borrowing rate. Paying off the percentage for the emmission of DAI in MKR token is a unique economic precedent in itself. This mechanics allows to avoid a typical concern with fiat money, when the debt of the central bank exceeds the amount of issued money. DAI emission system overrides this concern completely.

How you can use DAI and MakerDAO to your advantage right now

The use of MakerDAO emission mechanism can prove interesting for the purpose of crediting with ETH collateral, or receiving a decentralized credit leverage. Hence, having ETH 100 ($15,000), one can generate up to $9,000 in DAI that later can be spent to purchase some extra ETH.

DAI emission system can also become an accessible credit solution. With ETH as collateral, it will be possible to create a certain amount of DAI that will be reimbursed later from the future proceeds. With the interest rate of 2.5%, and the absence of banking commissions, MakerDAO might look like a decent alternative to a bank collateral credit line.

Is DAI to become a viable alternative to the ‘banking cartel’ of stablecoins?

Despite the technological innovation, durable lines of codes tested by the array of events at the crypto market, and respect of crypto enthusiasts, mass adoption of any decentralized financial product is no easy task. First off, since all of DAI are created under the ETH collateral, the total amount of DAI is restricted. If 10% of all the ETH is used as collateral, with the exchange rate of $150, only $939 mln DAI can be created. Of course, once ETH returns to the peak of its $1000 price, this amount will surge, yet it will still be insignificant on a global scale.

The second issue is liquidity and accessibility for sale-purchase. However, despite the recent listing of DAI and MKR on Coinbase, DAI is traded mostly against ETH. At the same time, it’s apparent that mass adoption of DAI, the entry and exit points into fiat are very much needed, since the majority of DAI use cases (like payments and crediting) would eventually require the exit to fiat. Yet, there is not so many options to sale-purchase DAI for fiat currencies – there are only two exchanges that have those trade pairs at the moment. One of them is Ethfinex, yet it cannot boast the most convenient ways to deposit and withdraw funds. The other one is EXMO, who recently announced support for DAI and MKR and introduced fiat pair to USD. Oddly enough, there are no more instances of DAI against fiat with non-zero liquidity at the market currently.

This is partially due to the fact that the majority of larger exchanges for apparent reasons would be way more interested in cooperating with institutional players rather than decentralized (i.e. completely independent) system of electronic cash flow. Therefore, despite some apparent advantages of DAI for an average user, such as transparency and independency of the third parties and all sorts of middle men, the competition with the banking cartels will be exceptionally strong. Still, DAI has apparently created a niche of its own that is bound to expand gradually, with restriction of total volume of issued coins and liquidity influx being the major factor contributing to its adoption in Web 3.0 ecosystem. Fast forward to today and we’ve witnessed the growing excitement in the space, with more than $70 million US dollars created in MakerDAO ecosystem, compared to only ~$3 million of the last year. Knowing that the cryptomarket has historically shown interest to vacant means of payment, we can only guess how many DAI will be generated and subsequently used one year from now.

Authors: Olga Grinina and Vasily Sumanov

Image(s): Shutterstock.com